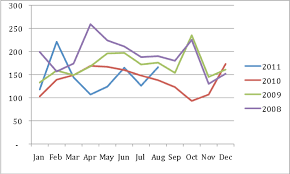

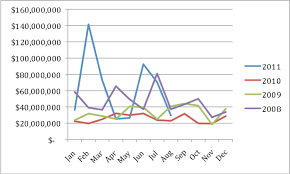

As the graphs show property sales are maintaining impressive growth this year over 2010’s numbers. Year to date sales volumes up to the end of August 2011 show a 203% increase over the same period during 2010. There has been a total of CI$422million transfers for 2011 compared to CI$207million for the same period during 2010, CI$255m for 2009 and CI$403million in the last boom year of 2008. Clearly this is positive news but if you drill down deeper there is still a contrasting trend in terms of the number of transactions which are in fact down 10% on last year’s numbers: There were only 1006 transfers in 2011 compared to 1173, 1350 and 1,602 in 2010, 2009 and 2008 respectively. This averages about 15% per annum drop in property transactions over the four year period and is a clear indication that whilst sales at the top end of the market remain solid, the number of sales at the mid to lower end have declined annually since 2008. In short this indicates that significantly less people buying lower to mid priced condominiums and development lots. CIREBA’s statistics which analyse sales by property type support this, showing a significant 50% drop in the number of home lots sold and 25% drop in the number of condominiums sold since the last boom year of 2008. Clearly this will not be too surprising to many, bearing in mind the reduction in population due to the cumulative effect recession staff cutbacks and immigration policies including rollover. The good news is that we appear to have turned the corner in relation to this particular policy as now both political parties appear to have come to the realisation that rollover, despite its best intentions, clearly doesn't work and any benefits it may have had were greatly outweighed by it’s negative effects on the economy. The other good news is that a number of the major projects on the cards appear to be moving forward - with one – the West Bay Road bypass even breaking ground. If we can keep up the momentum with the Shetty Hospital, the Airport and Port projects and the Enterprise City we should still be in good shaper during the years to come. In addition there appear to be two significant residential/resort projects for the Bodden Town area working their way through their due diligence processes and whilst these are some way off, the fact that developers are still moving them forward is a sign of confidence in the Cayman economy and real estate market. One challenge to any project that needs external international financing is that the rest of the world is looking to be in even worse shape than it was three months ago which will likely affect the availability of debt and equity financing into any major real estate projects. Whilst on a macro level is not good news, the flip side of this coin means that Cayman should continue be viewed as more attractive than many onshore jurisdictions….. so long as….. we can keep crime in check. The recent crime outbreak, whilst appearing to be largely contained to certain districts where crime has always been seen as more prevalent, will make it particularly difficult to achieve residential sales especially at the higher end of the market, whose owners may be trying to attract international investors. In general however we appear to have made good progress over the last quarter and so long as we can deal with local social issues, the outlook for the market still looks positive for the 2010/11 winter season and beyond. Jeremy Hurst – President?

Property Sales Volumes – CI$ – 2008-2011

Number of property sales transactions – 2008-2011